Deloitte Asset Servicers Survey 2023

The age of transformation

Asset servicers are innovating their operating models to tackle their clients’ evolving expectations and market challenges. Discover the current state of play and the trends shaping the industry’s future.

Asset servicers are evolving

With client expectations, cost pressures and regulatory requirements climbing, asset servicers are rising to the challenge by investing in emerging technologies and streamlining their core activities. Discover the findings in our 2023 report by Deloitte.

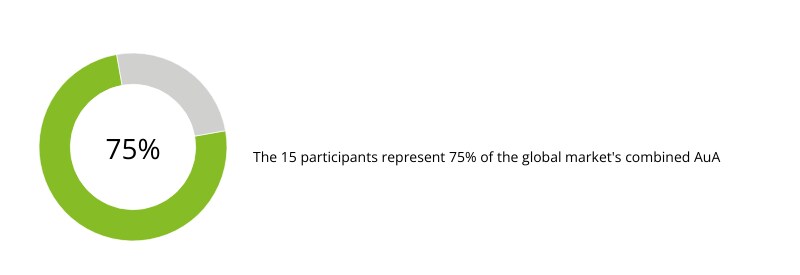

15 asset servicers with combined assets under administration (AuA) of more than $176 trillion headquartered in six different countries across EMEA (60%) and the US (40%) contributed to the 2023 Deloitte Asset Servicers Survey

The respondents are a representative sample of the industry covering a range of organizations, including those servicing traditional and alternatives or pure alternative players

AuA Data

AuA Data

Our analysis uncovered five key trends impacting the asset servicing industry: data and digitalization, innovation, operating models, alternative investments, and sustainability and ESG.

Data and digitalization

Data and digitalization

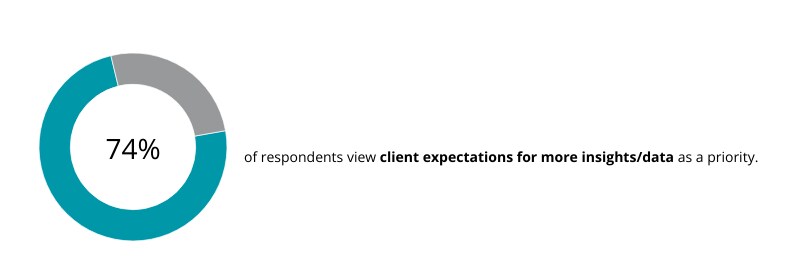

- Client expectations for further data and insights underlines need for digitalization of current operating models.

- Popular digitalization efforts include developing real-time self-service reporting models and live dashboarding capabilities.

Innovation

Innovation

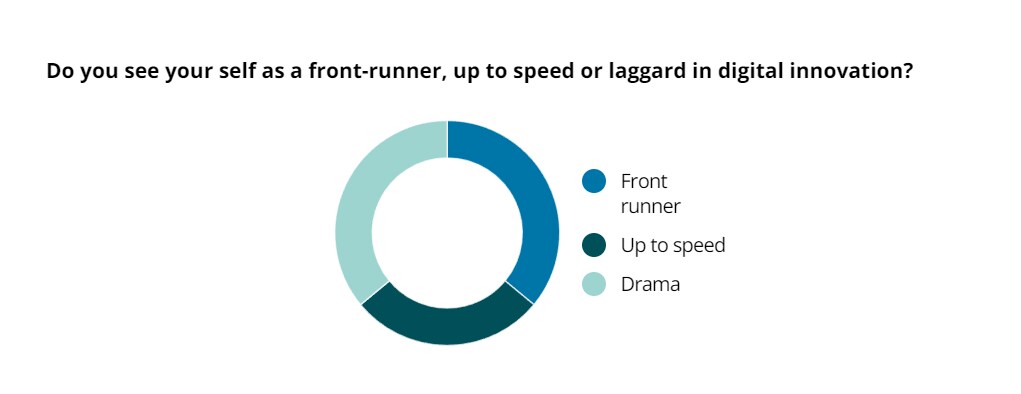

- 28% of asset servicers think they are front-runners in digital innovation and 36% of respondents believing they are laggards.

- Cloud projects are paramount, but often slowed down by regulations or group-driven directives.

Operating models

Operating models

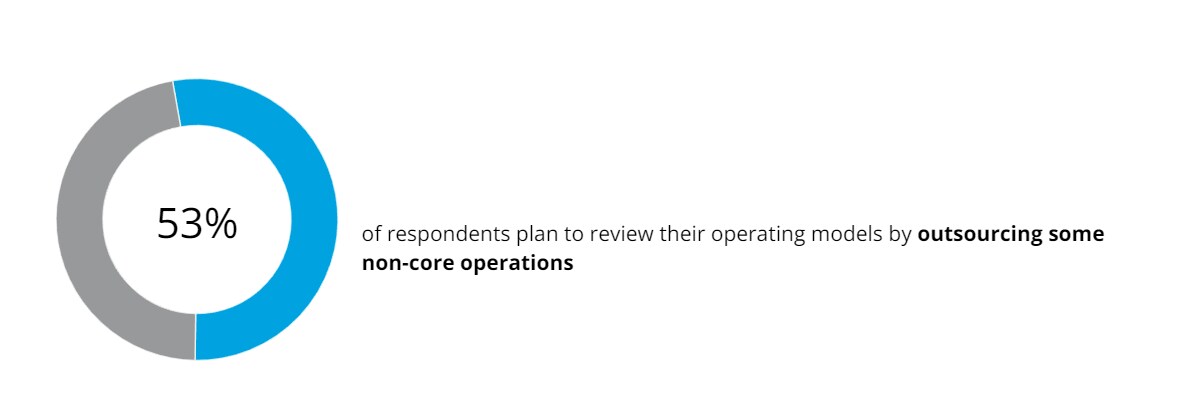

- Asset Servicers look at their Operating model and identify non-core activities and move further up the value chain by offering front-to-back solutions.

- 53% of respondents plan to review their operating model by outsourcing some operations.

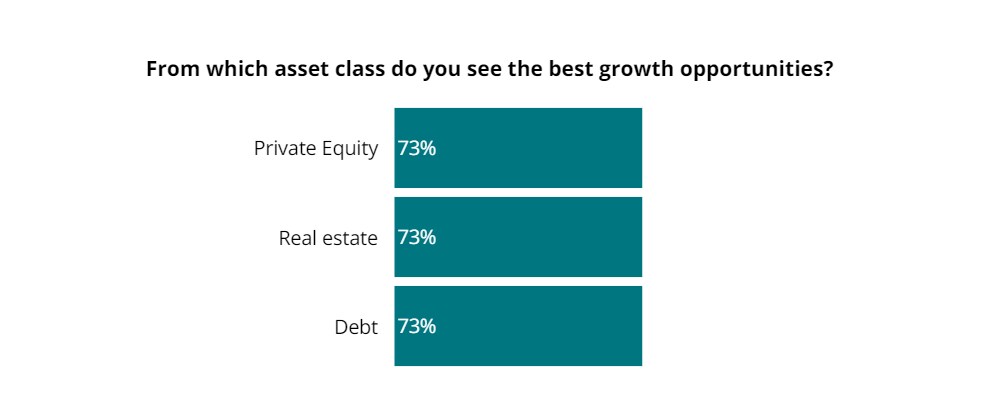

Alternative investments

Alternative investments

- A major revenue and margin contributor.

- 73% of respondents expect PE, RE and Debt products to drive the growth of their activities.

- Retail investors’ appetite for these assets continues to be strong and translates in the rise of demands for Hybrid funds.

Sustainability and ESG

- ESG requires significant and ongoing budget allocation by asset servicers. Reporting and data sourcing being the main areas of investment.

- There is clear room for improvement in the sector’s ESG reporting capabilities, with only 62% of respondents covering principle adverse impacts (PAI).

There is clear room for improvement in the sector’s ESG reporting capabilities, with only 62% of respondents covering principle adverse impacts.