Future in the balance? How countries are pursuing an AI advantage

Insights from Deloitte’s State of AI in the Enterprise, 2nd Edition survey

WITH leaders increasingly seeing artificial intelligence (AI) as helping to drive the next great economic expansion, a fear of missing out is spreading around the globe. Numerous nations have developed AI strategies to advance their capabilities, through investment, incentives, talent development, and risk management. As AI’s importance to the next generation of technology grows, many leaders are worried that they will be left behind and not share in the gains.

By measuring the global pulse of AI through our State of AI in the Enterprise, 2nd Edition survey, we uncovered four key insights from early adopters in seven countries:

There is a growing realization of AI’s importance, including its ability to provide competitive advantage and change work for the better. A majority of global early adopters say that AI technologies are especially important to their business success today—a belief that is increasing. A majority also say they are using AI technologies to move ahead of their competition, and that AI empowers their workforce.

AI success depends on getting the execution right. Organizations often must excel at a wide range of practices to ensure AI success, including developing a strategy, pursuing the right use cases, building a data foundation, and cultivating a strong ability to experiment. These capabilities are critical now because, as AI becomes even easier to consume, the window for competitive differentiation will likely shrink.

Early adopters from different countries display varying levels of AI maturity. Enthusiasm and experience vary among early adopters from different countries. Some are pursuing AI vigorously, while others are taking a more cautious approach. In some cases, adopters are employing AI to improve specific processes and products; others are harnessing AI to transform their entire organization.

Regardless of countries’ AI maturity level, we can learn from their approaches. By examining countries’ challenges and how companies there are addressing them, we can glean some essential leading practices. For example, leaders in some countries are more concerned about addressing skill gaps. Others are focusing on how AI can improve decision-making or cybersecurity capabilities.

There are many paths to AI excellence, and success is not a winner-takes-all proposition. Examining early AI adopters through a global lens can enable a broader perspective. By doing so, everyone can take a more balanced approach on their AI-powered journey.

AI advantage is not a zero-sum game

In the coming years, AI technology will exert an enormous impact on economic development and the nature of work. It will also radically reshape the competitive dynamics of many industries. Because of this, many leaders believe that their countries’ futures hang in the balance. It is no wonder that governments are rushing to foster AI investment, establish education programs, and pursue research and development to support businesses within their borders.

In fact, many governments have developed formal AI frameworks to help spur economic and technological growth. These range from the US executive order on AI leadership and China’s “Next Generation Artificial Intelligence Development Plan” to “AI Made in Germany” and the “Pan-Canadian Artificial Intelligence Strategy.”1 These strategies focus on talent and education, government investment, research, and collaborative partnerships. But governments face more than technological and economic challenges. Many are assessing how they can ensure privacy, safety, transparency, accountability, and control of AI-enabled systems without curtailing innovation and the potential economic benefits.

Notwithstanding intense competition among countries and companies, AI shouldn’t be considered a zero-sum game. All adopters can learn from one another, and early success will likely depend on getting the execution right—from choosing the right use cases, to preparing the workforce, to managing risks and challenges.

To better understand how early-adopter companies are navigating their AI journey and how they are beginning to transform, we surveyed 1,900 executives from around the world (see sidebar, “Methodology”). We also wanted to explore how AI is affecting their businesses—and whether there are distinct differences in how various countries are advancing their AI efforts.

Methodology

To obtain a global view of how organizations are adopting and benefiting from AI technologies, in Q3 2018 Deloitte surveyed 1,900 IT and line-of-business executives from companies that are early adopters of AI (prototyping or implementing AI solutions). Seven countries were represented: Australia (100 respondents), Canada (300), China (100), Germany (100), France (100), the United Kingdom (100), and the United States (1,100).

All respondents were required to be knowledgeable about their company’s use of AI technologies, and 91 percent have direct involvement with their company’s AI strategy, spending, implementation, and/or decision-making. Forty-seven percent are IT executives, with the rest line-of-business executives. Two-thirds are C-level executives: CEOs, presidents, and owners (31 percent); CIOs and CTOs (31 percent); and other C-level executives (4 percent). Thirty-four percent are executives outside the C-level.

To complement the blind survey, Deloitte also conducted an online, moderated panel discussion with AI transformation experts from various industries.

Taking the global pulse of AI

Do AI adopters from different countries vary in their practices? Are they just experimenting with AI, or using it to drive broader transformation and competitive advantage? What urgency do they feel amid their competitors’ actions? To answer these questions, we should first check the pulse of the global AI landscape.

Almost two-thirds of early adopters say that AI technologies are “very” or “critically” important to their business success today, increasing to 81 percent in just two years. In fact, four in 10 believe that AI will be critically important within two years. Much like the governments of the countries in which they operate, a growing number of organizations have strong feelings that AI will be essential to leading in the future. These adopters are using a variety of AI technologies, including machine learning, deep learning, natural language processing, and computer vision (see sidebar, “The AI technology portfolio”).

The AI technology portfolio

Machine learning. With machine learning technologies, computers can be taught to analyze data, identify hidden patterns, make classifications, and predict future outcomes. The learning comes from these systems’ ability to improve their accuracy over time without explicitly programmed instructions. Most AI technologies, including advanced and specialized applications such as natural language processing and computer vision, are based on machine learning and its more complex progeny, deep learning. Our survey shows 61 percent of global respondents using machine learning.

Deep learning. Deep learning is a subset of machine learning based upon a conceptual model of the human brain called “neural networks.” It’s called deep learning because the neural networks have multiple layers that interconnect: an input layer that receives data, hidden layers that compute the data, and an output layer that delivers the analysis. Deep learning is especially useful for analyzing complex, rich, and multidimensional data, such as speech, images, and video. It works best when used to analyze large data sets. New technologies are making it easier for companies to launch deep learning projects, and adoption is increasing. Among our global respondents, 51 percent said they use deep learning.

Natural language processing (NLP). NLP is the ability to extract or generate meaning and intent from text in a readable, stylistically natural, and grammatically correct form. NLP powers the voice-based interface for virtual assistants and chatbots. The technology is increasingly being used to query data sets as well.2 Sixty percent of global respondents have adopted NLP.

Computer vision. Computer vision is the ability to extract meaning and intent from visual elements, whether characters (in the case of document digitization) or the categorization of content in images, such as faces, objects, scenes, and activities. The technology behind facial recognition—computer vision—is a part of consumers’ everyday lives. For example, some mobile phones permit their owners to log in via facial recognition. Computer vision technology “drives” driverless cars and animates cashier-less stores.3 Computer vision has also gone mainstream with our global respondents, 56 percent of whom say their company uses it today.

There are indications that the window for competitive differentiation with AI is rapidly closing. As AI technologies become easier to consume and get embedded in an increasing number of products and services, the early-mover advantage will rapidly diminish. A majority (57 percent) believe that AI technology will substantially transform their company within the next three years (see figure 1). However, only 38 percent think AI will transform their industry in the same time frame. The perceived slower industry shift may represent a small window of opportunity. Early adopters may be wise not to underestimate their competition.

AI early adopters are aiming to improve both their external and internal capabilities. The primary AI benefits they report are enhancing products and services (selected by 43 percent as one of their top three benefits) and optimizing internal business operations (identified by 41 percent as a top-three benefit). Companies may choose an internal or external focus (or both), and many are pursuing a variety of use cases. For example, a panel member and retail CIO has explored a number of applications: “We have looked into a wide variety of use cases, starting with automation across all channels, chatbots to assist with customer inquiries, as well as decision support and customer analytics to better understand buying patterns and product performance.”

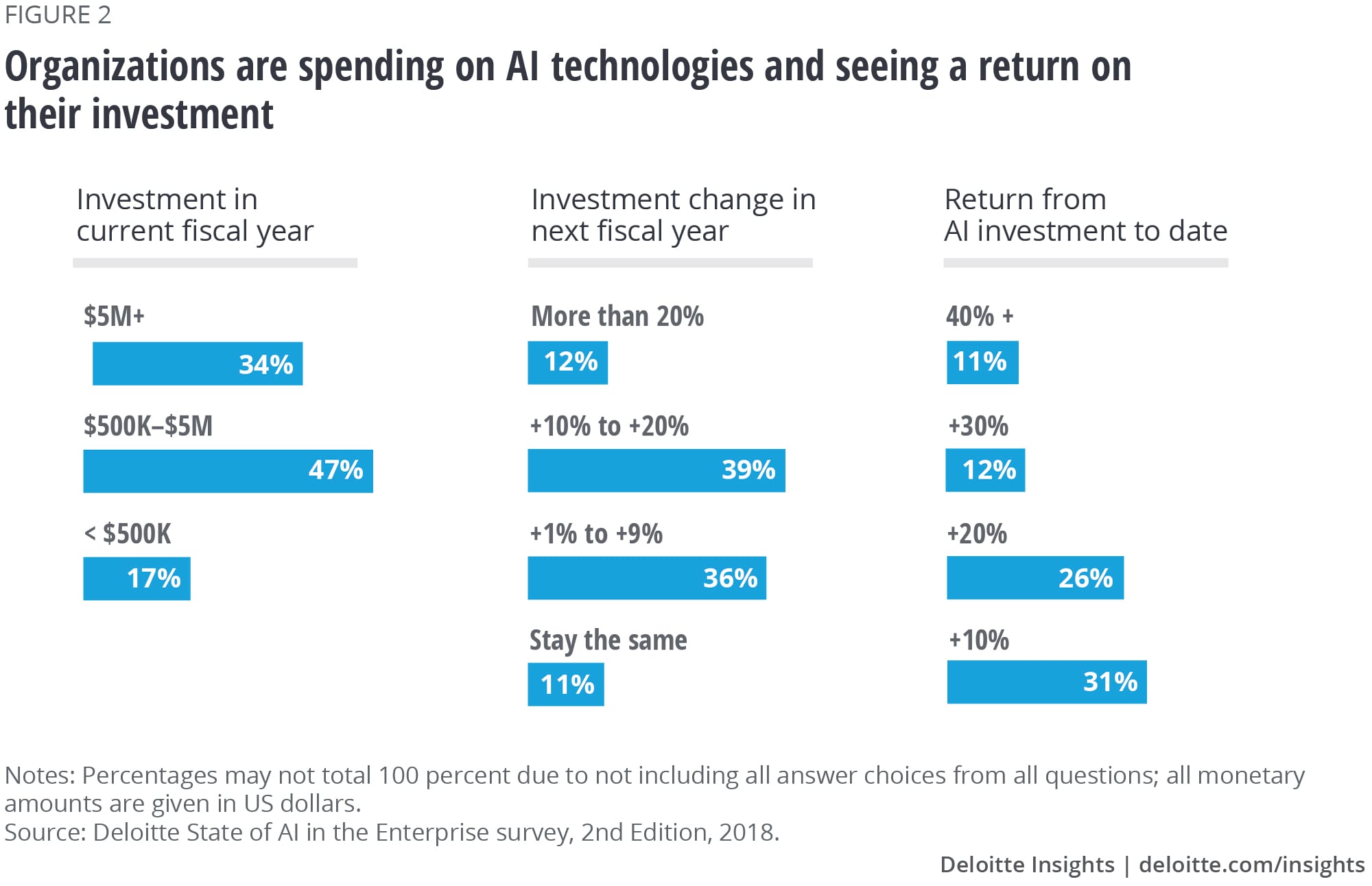

There are many estimates of total global AI spending, investment in AI startups, and the impact of AI technologies on the future economy.4 Most assessments agree that the United States and China are investing the most, with members of the European Union looking to quickly catch up.5 Rapid market growth is evident, and our respondents indicate they are increasingly spending on AI technologies and getting positive returns (see figure 2). In fact, 51 percent expect to increase their AI investment by 10 percent or more in their next fiscal year.

Even with a high level of excitement and willingness to invest in AI technologies, organizations are facing a set of interwoven challenges. Between 30 and 40 percent of our global sample identified the following challenges in their top three: integrating AI into roles and functions, data issues, implementation struggles, cost, and measuring the value of AI implementations. Carlo Torniai, global director of digital product development at Pirelli, has experienced a few of these. “Challenges most of the time have been related to data quality and availability, clear and measurable key performance indicators (KPIs), and resistance to change,” he explains. Every organization should think about these potential barriers ahead of time and make plans for how to address them.

Executives are also worried about broader vulnerabilities, with 43 percent saying they have major or extreme concerns about potential AI risks. Topping the list are cybersecurity vulnerabilities (49 percent rated it as a top-three concern) and making the wrong decisions based on AI recommendations (a top-three concern for 44 percent). Additionally, forty percent point to the potential bias of AI decisions as a top-three ethical risk. Falguni Desai, global head of strategy and transformation, equities, at Credit Suisse has concerns about trusting AI, “Regulators will need to get more involved if we are to have trust and transparency in AI, regardless of what type of use case—the same way we look for star ratings in travel, food grade levels, and testing before drugs go on market.”

Finally, most organizations face AI skill gaps and are looking for expertise to bolster their capabilities. Sixty-eight percent of global respondents indicated moderate-to-extreme AI skills gaps, and the top three roles needed to fill the gaps include AI researchers, software developers, and data scientists. Many companies are also looking beyond technical expertise, citing the need for business leaders who are able to interpret AI results and make decisions and take actions based on them. While organizations may believe that seeking the best external talent will provide an advantage, training their current workforce shouldn’t be overlooked. Jack Crawford, managing partner and CEO of Datalog.ai, suggests, “I’m in favor of education of senior management before establishing technical centers of excellence. Business needs to lead the charge, and leaders need to believe in order to drive the organization forward.” AI will change the way people work, and a spectrum of skills will be needed to ensure success.

Comparing perspectives

It’s illuminating to look at AI early adopters by country to assess the level of maturity they’ve reached, how they view the strategic importance of AI to their business, and how concerned they are about potential AI risks and challenges (see figure 3).

Maturity: Even though all respondents are early AI adopters, already prototyping or implementing AI solutions, AI maturity is still generally low across the board. Less than a quarter within each country qualified as Seasoned adopters (see sidebar, “Who are the ‘Seasoned’ AI adopters?”). The United States hits the high point at 24 percent of AI adopters classified as Seasoned. Strategic maturity—in terms of having a comprehensive, companywide AI strategy—is also still quite low, with China and the United Kingdom leading in this area.

Who are the “Seasoned” AI adopters?

Some adopters of AI are further along in their efforts than others. To aid our comparison, we identified three distinct segments at different levels of maturity. The “Seasoned” (21 percent of the global sample) are the most experienced AI early adopters, at the leading edge of AI adoption maturity. They have undertaken a large number of AI production deployments and report they’ve developed a high level of AI expertise—in selecting AI technologies and suppliers, identifying use cases, building and managing AI solutions, integrating AI into their IT environment and business processes, and hiring and managing AI technical staff. In the middle are the “Skilled” (43 percent). They have generally launched multiple AI production systems but are not yet as AI-mature as the Seasoned. They lag on their number of AI implementations, their level of AI expertise, or both. At the other end of the spectrum are a group of “Starters” (36 percent) that are just dipping their toes into AI adoption and have not yet developed solid proficiency in building, integrating, and managing AI solutions.

Urgency: The early adopters are anticipating rapid change. No matter their country, they resoundingly agree that AI is “very” or “critically” important to their company’s success today. A closer look reveals the percentage of executives rating AI as critically important will surge over the next two years—with some countries making a bigger leap than others (see figure 4). Additionally, a majority within each country believe that AI will transform their business within the next three years (see figure 3). China exhibits the greatest optimism, with more than three-quarters taking this view.

Even though the competitive landscape differs by country and industry, we wanted to understand whether early adopters use AI primarily to stay on par with peers or to create a competitive lead. Perspectives vary considerably. More than half of respondents from China (55 percent) believe they’re widening a lead over the competition or even leapfrogging ahead. Half of respondents from Australia say they’re using AI only to catch or keep up with the competition (see figure 5).

Challenges: Early adopters in various countries expressed contrasting levels of concern about AI risks. For example, about half of respondents from Australia and France reported a major or extreme concern, compared with just 16 percent of respondents from China (see figure 3). Some countries’ early adopters feel more “fully prepared” for these AI risks than their counterparts from other countries. In particular, respondents from Germany and China appear to have a surplus of confidence, with faith in their preparedness surpassing their level of concern (see figure 6).

Looking at specific challenges, a lack of AI skills seems to be a pervasive issue. Depending on the country, 51 to 73 percent of early adopters report moderate-to-extreme skill gaps (see figure 3). Another common challenge involves AI’s potential cybersecurity vulnerabilities. Across countries, at least four in 10 AI early adopters rate this as a top-three concern (rising to 54 percent in China).

A deeper view, by country

Australia: Trying to keep pace

Organizations from Australia hold a positive view of the strategic importance of AI to their success. Seventy-nine percent believe AI will be “very” or “critically” important to their business within two years. Despite the optimism, 50 percent of AI early adopters from Australia report that AI helps them “catch up” or “keep up” to their competition, rather than establish a distinct lead—the highest rate of all countries (see figure 5). It appears there’s a mismatch between perceived levels of urgency and readiness.

Inadequate AI strategies appear to be one impediment, with 41 percent reporting that their company either completely lacks an AI strategy or has only disparate departmental strategies (versus 30 percent globally). Skill gaps present another obstacle: A third of respondents from Australia, more than from any other country, called their AI skill gaps “major” or “extreme.” They indicated that their most acute needs are AI researchers, business leaders, and software developers. The good news is that the majority (59 percent) of organizations from Australia are already using AI-as-a-service technology, allowing them to tap into AI capabilities without needing to build their own infrastructure or establish specialized in-house expertise.

Potential AI risks present another worry, with 49 percent of early adopters reporting major or extreme concern—the highest level among countries. Indeed, several prominent Australian business and industry leaders are urgently asking for a national debate on the policies and regulatory and ethical standards needed to address the risks and challenges associated with AI.6

The Australian government is looking to advance the country’s AI capabilities and build on what early adopters have done. While there is not yet a dedicated national AI strategy, the government recently published “Australia’s Tech Future.”7 The plan touches upon the economic importance of AI, as well as skills shortages in AI and data science, as part of a broader discussion of opportunities presented by digital technologies. The 2018–19 national budget allocated AU$29.9 million over four years to boost the country’s AI capabilities, including the development of a technology road map and frameworks for standards and AI ethics.8 However, AI experts are issuing warnings that greater levels of spending will be needed for Australia to keep up with other countries that are lavishing public funds on AI initiatives.9

Canada: Taking a cautious approach

As organizations pursue transformation with AI, they enter a new frontier of opportunity and risk. By unlocking operational efficiencies and new revenue streams, they confront a host of issues regarding ethical implications, enhanced cyber vulnerabilities, and questions of talent readiness. For Canadian enterprises, these new complexities are clearly at the forefront. For instance, 48 percent of early adopters from Canada cited “making the wrong strategic choice based on AI recommendations” as a top-three AI risk (highest among all countries).

Both today and in the near future, these concerns could throttle the pace of AI-driven innovation in Canada. To illustrate, consider two specific phenomena:

- A lack of urgency. Over a three-year horizon, only 51 percent of executives from Canada believe AI will transform their company (tied for the lowest rate among countries surveyed; see figure 3). Further, only 5 percent see AI as critically important to their business’s success today, increasing to 27 percent in the next two years (see figure 4).

- Slower innovation. Twenty-five percent of executives from Canada indicate they currently embed AI into their products and services—once again the lowest of all countries. Patent data bears this out: Since 2016, most countries accelerated their rate of AI-related patents, while Canada’s has decreased each ensuing year.10

As other organizations pursue AI strategies that fuel innovative products and services, Canadian companies are at risk of being left behind.11 Still, there is good news: At the national level, the country is making a concerted effort to bolster its collective AI capabilities. This is especially true for talent, where the government has put forth policies to make immigration an easier, more open process for those with AI-related skill sets.12 Perhaps this is one reason 68 percent of organizations from Canada—more than any other country—look outside their companies to enhance their talent pool.

While Canadian companies are clearly well positioned to focus on external sources of talent, attention should also be given to internal pools of talent. Respondents from Canada are less focused on training their workforces to develop and deploy new AI solutions. They report the lowest rate of training developers to create new AI solutions and IT staff to deploy AI solutions. One opportunity may be to partner with academic institutions like the University of Toronto, which is making a significant investment (upwards of CAN$100 million) to support the work of AI scientists, biomedical researchers, and even its entrepreneurship network to foster a more dynamic AI business landscape.13

By taking a more balanced approach, one that concurrently imbues new skill sets and strengthens the current talent pool, a more well-rounded workforce can emerge—one that empowers the entire organization to better navigate AI-related risks and simultaneously drive new product solutions.

China: Pursuing a strategic imperative

The Chinese government has declared its ambition for China to become the world’s leading AI innovator by 2030.14 It has published a national AI strategy and announced plans to invest tens of billions of dollars in AI research and development.15 Cities are also opening their coffers: Beijing announced a US$2.1 billion AI-centric technology park, and Tianjin plans to set up a US$16 billion AI fund.16 Money is flowing from the private sector, too: In 2017, Chinese AI startups received 48 percent of global AI venture funding, outpacing the United States for the first time.17 China reportedly has the world’s second-highest number of AI companies, behind the United States—and is home to the world’s most highly valued AI company, SenseTime Group Ltd.18

Our survey revealed that early adopters are embracing the Chinese government’s AI call to action:

- Key to success. Fifty-four percent consider AI to be “very” or “critically” important to their business success, and that is expected to grow to 85 percent in two years—the highest level across countries (see figure 3).

- Competitive edge. They are more likely to believe that AI is helping to widen a lead or leapfrog their competition (55 percent versus 37 percent globally; see figure 5).

- Improving the workforce. More than eight in 10 believe that human workers and AI technologies will augment each other to produce new ways of working, that AI empowers their employees to make better decisions, and that AI technologies will enhance employee performance and job satisfaction.

Despite the exuberance, China has the smallest proportion of organizations (11 percent) that fall into our Seasoned category (see figure 3). In light of this relative lack of maturity, the surplus of confidence about preparedness for AI risks (see figure 6) and the majority belief they’re leapfrogging the competition may be signs of overconfidence. Recognition of the risks and challenges is likely to grow as AI experience increases.

Although not as far along in AI adoption, organizations from China are demonstrating signs of strategic maturity by putting policies, procedures, and metrics in place to succeed with AI. Almost half (46 percent) indicate they have a comprehensive, organizationwide strategy for adopting AI—the highest rate among countries studied. And 62 percent have already established a companywide process for determining how AI prototypes get moved into production—again outpacing all others. Early adopters from China are also more keenly tracking performance metrics of their AI initiatives.19

Although the AI revolution has been proceeding rapidly in China, there may be bumps ahead. After reaping the largest share of global AI funding in 2017, China’s share dipped in 2018.20 Chinese AI companies tend to be heavily application-focused and place less emphasis on advancing foundational technologies and research, which could prove limiting to growth.21 At the same time, in a quest for ever more computing power to run sophisticated AI algorithms a number of Chinese tech companies are designing and even build their own AI-optimized chips.22

France: Aspiring to empower people

In 2017, President Emmanuel Macron appointed mathematician Cédric Villani to develop a national AI strategy. The next year, “AI for Humanity” was released and €1.5 billion earmarked to enact the plan’s recommendations.23

The plan details how to align the country’s resources around talent, an open data ecosystem, research institutions, and the ability to address ethical issues and enhance specific sectors of the French economy. The government is making it a priority to develop AI both domestically and by working broadly with the European Union. This overall optimism is evident in our study, as most early adopters from France (76 percent) agree that AI will help augment human capabilities, enabling a collaborative working partnership.

However, despite the optimism, AI early adopters signal they are starting gradually in their quest for AI-driven transformation. In terms of AI adoption maturity, we classified 51 percent of respondents from France as Starters, the highest proportion among all the countries surveyed (see sidebar, “Who are the ‘Seasoned’ AI adopters?”). Additionally, 45 percent are undertaking smaller AI projects targeted at specific functions, the highest rate among countries. Large-scale, transformational projects are not yet a priority—there may be other competing priorities, including General Data Protection Regulation (GDPR) compliance and broader data management efforts. Finally, many companies feel their AI deployments are simply enabling them to keep up with their competition (see figure 5).24

Organizations may feel headwinds from people challenges as well as the technical challenges of adopting AI. Our survey reveals that adopters in France are struggling to obtain talent and to integrate AI into their organizations’ processes. Their top challenge is difficulty integrating AI into roles and functions, with 45 percent—the highest rate among countries—selecting it as a top-three challenge. Thirty-one percent of respondents said they have major or extreme skill gaps, the second-highest rate among countries surveyed. As outlined in “AI for Humanity,” the French government would like to address this and develop and support a vibrant AI ecosystem powered by graduates of the French education system.25

To support the aims of the French government, organizations can focus on their people problems, look for ways to alleviate the stress of keeping up, and seek tools to accelerate their AI journey. One way to fast-track efforts is to use easy-to-consume AI solutions, such as cloud-based as-a-service applications. We found that early AI adopters from France are primarily pursuing AI-embedded enterprise software (57 percent) and open-source solutions (56 percent). An example of this focus is seen in France-based startup Dataiku, which is helping drive enterprise AI adoption by providing open-source solutions on its platform.26

Germany: Turning fears into strengths

The German government is looking to accelerate the adoption and development of AI technologies. As a result, it is planning to invest €3 billion in AI research between now and 2025 to help implement its national AI strategy (“AI Made in Germany”).27 Like many countries, Germany hopes that adopting AI will expand its broader economy and improve the competitiveness of its existing industries. A recent study commissioned by the German government estimates that AI technology could add €32 billion to the country’s manufacturing output.28 Germany’s strategy is holistic, emphasizing not only improved competitiveness but the responsible use of AI and its impact on the German workforce.

AI early adopters from Germany stand out in a unique way, as they appear to be dealing more with some of the ethical concerns surrounding AI than those from other countries. Their top ethical concern is using AI to manipulate information and create falsehoods; 47 percent selected it as a top-three ethical concern. They are also worried about potential job cuts from AI-driven automation, with 43 percent rating it a top-three issue, tied with France for the highest among countries. Germany also has the lowest percentage of respondents agreeing their company wants to automate as many jobs as possible with AI. This isn’t surprising, as officials in Germany—with its strong economic focus on engineering and manufacturing—have been concerned about the impacts of automation in every era, including the digital age.

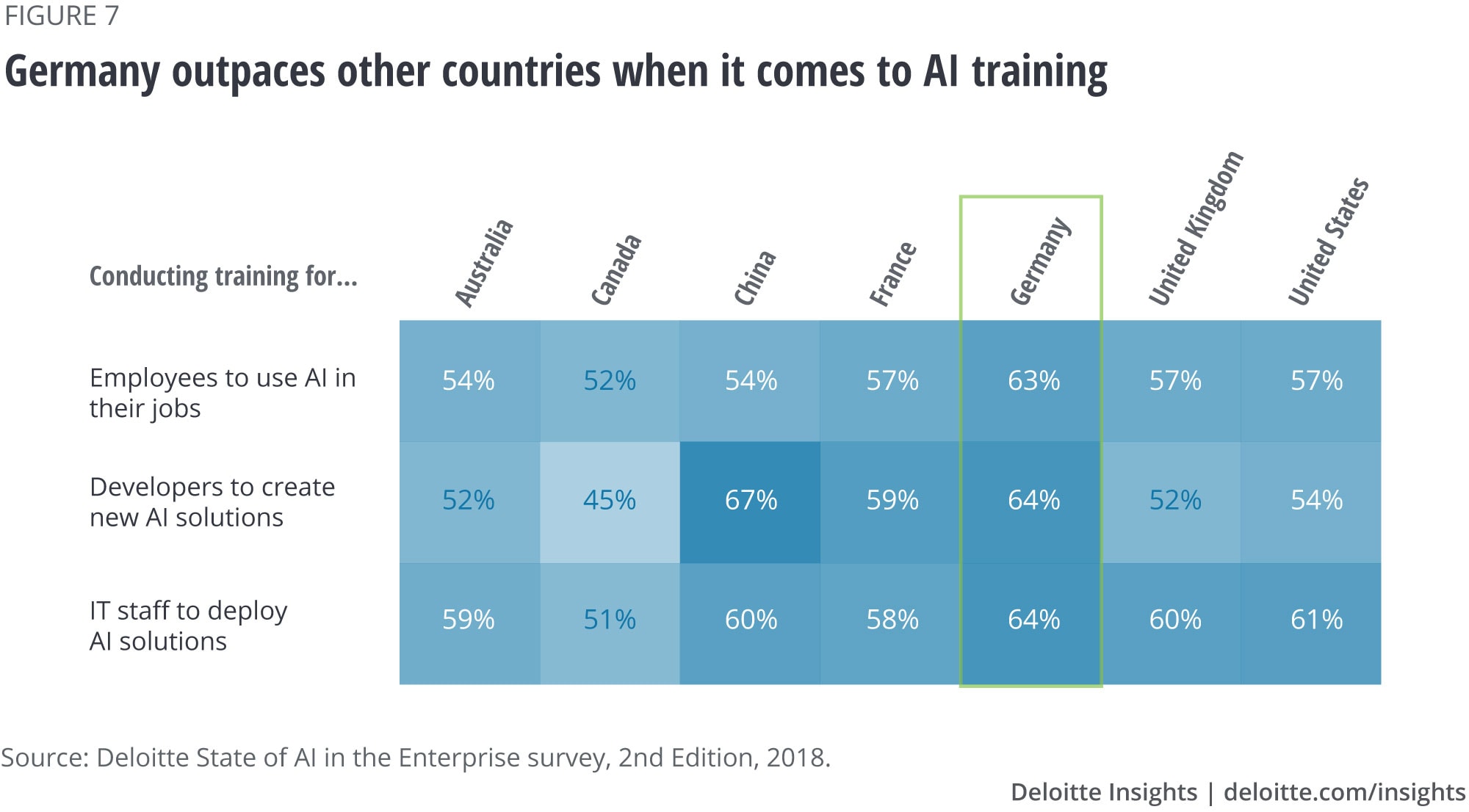

The good news is that AI adopters from Germany indicate a strong focus on AI training (see figure 7). They tend to have a more tempered view of AI’s ability to enhance job performance and enable new human/machine partnerships, but they report stronger efforts around employee education. Respondents from Germany are more likely than their counterparts from other countries to train employees to use AI in their jobs, train developers to create new solutions with AI, and train IT staff to deploy these solutions.

This holistic approach to filling the AI talent gap is a source of advantage, and one from which other countries can learn. Organizations shouldn’t worry only about acquiring and educating a new generation of AI experts—they also should develop and retrain existing workforces. Leaders may also wish to explore how ensuring ethical AI can become a source of competitive advantage. For example, SAP has set up an advisory panel drawn from government, industry, and academia to help drive a set of principles for the company’s AI work.29

United Kingdom: Betting big on the future of AI

The United Kingdom is an enthusiastic participant in the global AI revolution, with a thriving AI startup scene and £1 billion of government support for industry and academia.30 But what about UK organizations that are already early adopters of AI?

First, there is a strong recognition of the increasing importance of AI and a corresponding near-term investment. Respondents from the United Kingdom show clear enthusiasm, with 45 percent saying AI will be of critical importance to their near-future success. They are backing up this exuberance with investment: 60 percent of respondents expect to increase their AI investment more than 10 percent next fiscal year. This is the highest rate for both of these measures among all countries surveyed (see figure 8). Although only 15 percent fall into the Seasoned category, organizations are feeling the pressure to move faster.

For these organizations to improve their chances of success with AI, they should channel their enthusiasm. And respondents appear to be going big with their approach to AI: They are more focused on undertaking large-scale, transformational AI initiatives than those from other countries. Twenty-nine percent are pursuing only large-scale initiatives; another 53 percent have a mix of focused and broader AI projects. UK companies also rank second in having a comprehensive strategy in place for AI adoption (with 41 percent). This may mean respondents feel the need to be more ambitious with their projects amid intense global competition.

To gain an AI advantage, it is essential to address challenges and risks early. Whereas some in the UK government are worried about legal liability, criminal misuse, and the impacts of autonomous decision-making, respondents have more practical concerns.31 Their top challenges include measuring and proving the business value for AI projects—the highest rate, with 45 percent ranking it a top-three challenge—and integrating AI into roles and functions; 41 percent rank it a top-three.

United States: Managing the complexity that comes with sophistication

For years, the United States has been a leader in public and private AI research.32 Consider the last several years of venture capital investment in the AI sector. In 2012, venture capitalists funded US$282 million in AI initiatives, and that number skyrocketed to US$5 billion by 2017. The following year, AI investments by VCs topped US$8 billion.33

This wave of investment helped transform many US organizations into relatively sophisticated AI users. For instance, 30 percent of respondents from the United States—highest of all countries—currently manage 11 or more AI production systems. And in our analysis of Seasoned AI early adopters (see sidebar, “Who are the ‘Seasoned’ AI adopters?”), US enterprises lead the field with 24 percent of respondents. It’s not just the quantity of production environments, either: More than a quarter (27 percent) of respondents from the United States indicate they are implementing at least one large-scale AI project, second only to the United Kingdom.

One might assume that early adoption implies mastery. However, our analysis reveals that sophistication brings about a greater recognition of the complexities that come with large-scale AI implementations.

Fully half of respondents from the United States view cybersecurity as a top concern (see figure 3). As organizations rely upon more and more data to fuel their enterprisewide AI initiatives, the stakes for protecting this information increase. Absent a clear strategy to address this issue, many potentially high-impact AI initiatives are at risk of slowing down or, worse, never getting off the ground. Our respondents highlighted two areas of concern:

- Protecting institutional data. Forty-seven percent of respondents from the United States are concerned about proprietary or sensitive data being stolen.

- Influencing AI models. Beyond theft, 45 percent of US executives worry that outsiders will influence training data and algorithms—directly skewing AI recommendations and insights.

As more companies weave AI into their operations and products, they increasingly need the right talent to support large-scale initiatives. But as the number of AI applications increases, the talent pool may feel somewhat fixed. Clearly, US organizations feel this pressure, as 68 percent perceive the talent gap as moderate-to-extreme (see figure 3).

In response to this talent pressure, many US enterprises are using internal training programs to bolster their workforce. Addressing the need for skills is becoming a more holistic effort, focusing not only on upskilling IT staff to deploy solutions (61 percent) but on teaching frontline employees how to integrate AI into their work (57 percent) (see figure 7). As AI initiatives permeate the organization, it’s paramount that the entire organization can work effectively with these new capabilities.

Conclusion: Taking a balanced approach

Governments will continue to invest in AI and monitor the technology’s ongoing impact on their societies. Businesses will continue to improve their AI capabilities and make them central to their competitiveness. Both will continue to feel a sense of urgency and anxiety as they try to keep up with the rapid pace of AI-driven developments around the world. In light of this, organizations should confront a series of vexing questions when evaluating their AI strategies:

- Should they make small, incremental investments or try to position themselves as AI leaders through enterprisewide initiatives?

- Is it better to develop existing talent or seek help from the external talent market?

- When considering the inherent risks associated with AI, should organizations proceed in the face of complexity or take a slower, more cautious approach?

Our survey reveals that, no matter where organizations are on their AI journeys, their approach to tackling these questions varies. Some are playing catch-up with their global rivals. Others are addressing their aims through focused projects, or by pursuing larger-scale initiatives. Some early adopters are much more focused on training and skills development than others. Even those that have comprehensive, mature AI strategies are approaching execution differently.

There are many paths to AI excellence. By taking a step back and examining AI early adopters through a global lens, we can enable a broader conversation and help countries learn from one another. By doing so, all can take a more informed, balanced approach to pursuing their unique AI advantage. Consider the following:

Balance caution and action

- Create a sense of urgency in your organization around AI—there is a small window for competitive differentiation.

- Respect the risks of AI, and don’t rush into a potential misstep just to keep up. There are dangers with both moving too slowly or quickly. Let your strategic business priorities help guide you.

- Build a strong foundation for an AI-powered future with effective practices for data management, experimentation, operational discipline, and talent development.

- Explore how other countries are facing their AI-related concerns. All have unique approaches to addressing cybersecurity fears, managing ethical questions, building trust in AI systems, and developing talent.

Balance the scale of your efforts

- Don’t be afraid to be ambitious. Even if you’re playing catch-up, AI initiatives need not always start small.

- To enable a more transformative approach with AI, pursue a diverse portfolio of projects that will enhance multiple business functions.

- Explore ways to ramp up AI capabilities quickly (for example, with cloud-based AI services or partnerships), rather than focusing exclusively on trying to do everything on your own.34

- Plan for the fact that, over time, AI will become easier to acquire, with smaller demands for in-house infrastructure, data requirements, and expertise.

Balance your approach to talent

- Though most are looking to the external market to build their AI expertise, opportunities abound to train and utilize existing employees. Build an education plan to identify and prepare current developers, IT staff, and other employees that could help advance your AI efforts.

- Take a holistic approach and improve both technology and business talent to support your AI strategy.

- Develop structured ways to integrate AI into roles and functions—and be prepared to evolve them for the future. Create a vision for what your “augmented workforce” looks like.

There's clearly no one-size-fits-all approach to adopting and integrating AI. AI-fueled transformation of businesses and industries appears to be coming rapidly, and the window for differentiation is shrinking. Much hangs in the balance—including the future competitiveness of companies and even whole countries. By combining enthusiasm with a balanced approach to AI goals and execution, companies and countries may find success.

The Center for Technology, Media & Telecommunications

Deloitte's Center for Technology, Media & Telecommunications (TMT Center) conducts research and develops insights to help business leaders see their options more clearly. Beneath the surface of new technologies and trends, the Center's research will help executives simplify complex business issues and frame smart questions that can help companies compete—and win—both today and in the near future. The Center can serve as a trusted adviser to help executives better discern risk and reward, capture opportunities, and solve tough challenges amid the rapidly evolving TMT landscape.

Learn more

{kind=link}

{kind=link}